In our last article, we unpacked cap rate and NOI as the starting point for evaluating commercial real estate investments in Fremont, Silicon Valley, and the greater Bay Area. Cap rate gives you a snapshot of risk and return of the first year of investment.

Internal rate of return (IRR) answers a more advanced question:

“Given all of the cash in and cash out over my entire hold period, including my eventual sale, what is my annualized return on this deal?”

Understanding IRR is essential for comparing deals and making long-term decisions for investors, family trusts, and business owners building CRE portfolios of industrial, warehouse, office, flex/R&D, or lab space.

To watch it as an 18-min video

To listen as an 18-min podcast

Here is a simply way of explaining IRR:

Corporate Finance Institute describes it as the expected compound annual rate of return on an investment.

Investopedia describes IRR as the rate at which net present value (NPV) of future cash flows equals zero — a standard definition across finance.

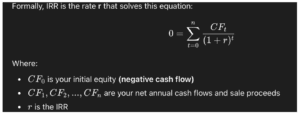

At its core, IRR is the discount rate that makes the NPV of all your projected cash flows (income and sale proceeds, minus your initial investment and capital costs) equal zero.

For commercial real estate specifically, IRR is “the percentage rate earned on each dollar invested for each period it is invested,” applying the time value of money to property cash flows. (Commercial Real Estate Loans)

From our prior cap rate article for Fremont and Silicon Valley investors:

Key differences:

In practice, sophisticated investors use cap rate to screen deals quickly, then use IRR to decide how and where to allocate capital.

Without a simple algebraic solution for most real-world deals, investors let Excel or financial calculators do the work:

From a decision standpoint, the classic rule is that a project is attractive if its IRR exceeds your minimum required return, often called your hurdle rate or cost of capital. (Investopedia)

Imagine a Fremont industrial condo or small warehouse:

If you plug these cash flows into an IRR or XIRR function, you might see an IRR in the low-to mid-teens: meaning your equity effectively compounds at roughly that rate over the full five-year hold.

Change the timing and shape of the cash flows, and you change the IRR — sometimes dramatically.

IRR rewards earlier cash flows and penalizes later ones, and this is both the strength and weakness of IRR.

Black Diamond Realty illustrates this with examples: investments with similar total profits can have very different IRRs if one produces cash earlier (leased quickly, minimal downtime) and another back-loads profits at sale. (Black Diamond Realty)

For CRE investors, that means:

This is why many investors establish a “hurdle rate” — the minimum IRR they’re willing to accept given their risk tolerance and alternative opportunities. (Black Diamond Realty)

In commercial real estate, IRR is used at several levels:

Sites like CommercialRealEstate.Loans show how investors use IRR to compare deals of different sizes and structures over a multi-year hold. (Commercial Real Estate Loans)

For example, you might compare:

IRR helps you see whether the extra risk and complexity justify the higher projected return, especially if your real objective is wealth preservation and stable income.

At the institutional level, IRR is also calculated across entire funds or portfolios.

Fund-level IRR helps compare strategies, sponsors, and vintages, especially from the perspective of limited partners (LPs) and general partners (GPs). (Built)

At the same time, institutional investors track performance against indexes such as the NCREIF Property Index (NPI), which measures property-level returns for core institutional assets across the U.S. (NCREIF)

For a private investor or family trust, you don’t need that level of infrastructure — but the principle is the same:

IRR is one of the key metrics professional investors use to judge manager performance, strategy quality, and portfolio construction.

IRR is powerful, but it is imperfect. Your underwriting will be stronger when you understand its weaknesses.

Traditional IRR implicitly assumes that interim positive cash flows can be reinvested at the same IRR, which is rarely true in the real world. Both Investopedia and CommercialRealEstate.Loans flag this as a core limitation. (Investopedia)

If your cash flow stream switches sign more than once (e.g., additional big capital injection midway through the hold), you can end up with multiple IRRs or none at all. Corporate Finance Institute and others note this issue in capital budgeting analysis. (Corporate Finance Institute)

IRR is percentage-based and can be misleading when comparing deals with very different sizes of equity or profit. CommercialRealEstate.Loans points out that a small investment with a very high IRR may be less meaningful than a much larger investment with a slightly lower IRR. (Commercial Real Estate Loans)

As said earlier, front-loading cash flow tends to boost IRR, which can over-reward short-term flips or aggressive assumptions about lease-up and rent growth. (Black Diamond Realty)

Professional investors evaluate projects with multiple metrics such as IRR, equity multiple (see 9 below), cap rate, NPV, and benchmark comparisons, instead of a single number. (Investopedia)

To address some of IRR’s weaknesses, many analysts look at MIRR (Modified Internal Rate of Return).

According to CommercialRealEstate.Loans: (Commercial Real Estate Loans)

For sophisticated CRE investors, running both IRR and MIRR can highlight how sensitive your projected returns are to your reinvestment opportunities and financing costs.

In practice, we recommend investors view IRR as one piece of a larger toolkit:

Together, these metrics help you answer:

For owners, investors, and operators focused on Fremont and Silicon Valley — especially in industrial, warehouse, R&D, and related sectors — here is how we suggest using IRR:

Our role as a commercial real estate advisor is to demystify metrics like IRR and tie them back to real-world decisions:

If you are considering buying, selling, or repositioning commercial property in Fremont, Silicon Valley, or the broader Bay Area, a clear understanding of IRR is one of the tools that will help you make more confident, better-informed decisions.

👉 To learn more, you can access, for a small fee, case studies: https://theivygroup.com/courses

👉 Subscribe to The Ivy Group newsletter: https://theivygroup.substack.com/

📩 Contact The Ivy Group: https://theivygroup.com/contact-us/

The Ivy Group specializes in commercial sales, leasing, and investment advisory across Fremont, Silicon Valley, and the Greater Bay Area. With over 100 years of combined experience and designations including SIOR and CCIM, The Ivy Group provides strategic guidance for complex transactions in commercial real estate. When you need to sell, buy, or lease, The Ivy Group is ready to help you reach your goals. Contact us with your next real estate needs.

All information shared here in this article, and in all blogs, case studies, and courses offered by The Ivy Group are for general education only, not as tax, legal, or investment advice. Please seek professional advice from tax, accounting, legal, and other professionals.

Copyright © 2025 by Tim Vi Tran, SIOR, CCIM. All rights reserved.