In Part 1, “1031 Exchange: How Savvy Investors Keep More Capital Working with This Tax Deferral Tool”, one area we discussed, among others, was “Tax Basis Step-up Erases Capital Gains Tax and Depreciation Recapture”.

In Part. 2, “Boot Tax and Estate Tax for 1031 Exchange Properties”, we zoomed in on boot tax related to 1031 Exchange properties.

Here in Part 3, we will wrap up boot tax issues: (1) How does the IRS prioritize ordinary income tax, capital gain, cash boot, debt boot, and non-like-kind property? (2) Why is boot not automatically “bad”, and when can it be strategically smart?

To watch this as a 13-min video

To listen to it as a 13-min podcast

All information shared here in this article, and in all blogs, case studies, and courses offered by the Ivy Group are for general education only, not as tax, legal, or investment advice. Please seek professional advice from tax, accounting, legal, and other professionals.

At the end of Part. 2, we mentioned that sometimes the perfect tax deferral is not worth chasing. It comes down to whether you want to maximize deferral or optimize portfolio fit. Sometimes the perfect tax deferral isn’t worth chasing if the asset trade is strategically better with a little boot.

The IRS has a priority order regarding which portion of boot is taxed first and how:

Here is an example:

Where the boot lands tax-wise matters. Here is a tax rate impact estimates (e.g., what $50K of boot looks like under ordinary vs. capital gains treatment):

| Boot Amount | Tax Treatment | Tax Rate (example)

** Tax rate depends on each individual bracket *** |

Estimated Tax Due |

|---|---|---|---|

$50,000 |

Ordinary Income (depreciation recapture) |

35% |

$17,500 |

$50,000 |

Capital Gain |

20% |

$10,000 |

The spread between ordinary vs. capital treatment grows fast as boot increases.

Now we address when it makes sense to avoid boot entirely, when it’s actually smart to take some boot, and how to soften the tax hit:

When to avoid boot (maximize deferral):

When boot can be strategically smart (flexibility or liquidity):

Ways to soften the tax hit:

Depending on your unique circumstances, you can either stretch to stay “pure 1031”, or accept a little boot and use it wisely.

How much cash you actually keep depends on whether the boot is taxed as ordinary income or capital gain, and your bracket.

Here is the “2/3 Rule of Thumb” that helps frame whether the liquidity you gain is worth the deferral you give up: Every $1.00 of boot leaves you with somewhere between $0.63–$0.80 in pocket, depending on how it’s taxed.

Use this shortcut test when sizing up the boot, and ask yourself:

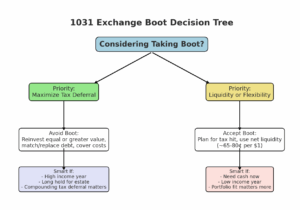

Here is a visual decision tree you can use as a gut-check for handling boot in a 1031 exchange, it helps you quickly see whether to lean toward avoiding or accepting it, based on your priorities and tax situation:

Below is a step-by-step checklist you can run through during a deal so boot doesn’t sneak up on you at closing. Use it before, during, and after a 1031 Exchange:

Think of it as a guardrail: if you check every box, you either avoid boot or at least take it with eyes open. Consulting your tax advisor is highly recommended.

The 1031 Exchange remains one of the most powerful tools available to commercial real estate investors, but only when executed with discipline and the guidance of a seasoned commercial real estate advisor.

Tax deferral improves cash flow that compounds your investment power, but it is rarely a one-size-fits-all solution. The decision to avoid boot or pay for it in a wise way depends on your own priority and circumstances such as the need for liquidity or flexibility, and your strategies to adapt, diversify, and change portfolios in response to market conditions.

It is best to navigate the strict IRS rules with experienced advisors’ professional guidance due to the sizable financial stakes. To avoid an expensive misstep, it is important to work with experienced commercial real estate advisors such as the Ivy Group, qualified intermediary, tax advisors, and legal professionals to accomplish a seamless 1031 exchange.

===================================

A commercial real estate transaction is a multi-faceted process that involves factors such as investment insights, financing, alignment of properties with clients’ specific needs, market analysis, savvy negotiation, communication, tax planning, and other related areas such as accounting, law, technology, and engineering.

Listing the rules is straightforward; applying them to specific cases is more complex.

In Part 2, we analogized it to playing basketball, learning all the rules of the game won’t get you anywhere, you need to practice over and again on the court. To win a game requires so many factors beyond experience: mental focus, teamwork, strategies, quick reaction, understanding the big picture, flawless execution, planning the details ahead…

To learn how these 1031 Exchange and related rules are applied in unique situations with moving targets and various puzzle pieces, you can access, for a small fee, case studies:

👉https://theivygroup.com/course-category/deal-structure-1031-exchange/

The Ivy Group specializes in commercial sales, leasing, and investment advisory across Fremont, Silicon Valley, and the Greater Bay Area. With over 100 years of combined experience and designations including SIOR and CCIM, The Ivy Group provides strategic guidance for complex transactions in commercial real estate.

👉 Subscribe to The Ivy Group newsletter: https://theivygroup.substack.com/

When you need to sell, buy, or lease, the Ivy Group is ready to help you reach your goals with more than 100 years of combined experience and expertise. Contact us with your next real estate needs.

All information shared here in this article, and in all blogs, case studies, and courses offered by the Ivy Group are for general education only, not as tax, legal, or investment advice. Please seek professional advice from tax, accounting, legal, and other professionals.

Copyright ©️ 2025 by Tim Vi Tran, SIOR, CCIM. All rights reserved.